Dr. Doug Cardell

An Eclectic Economist Explains Evidentiary Economics

Clear Thinking in a Complicated World

“Ideology asks for acceptance—Intelligence asks for evidence.”

Why Socialism Struggles

Buy the BookFeatured Article:

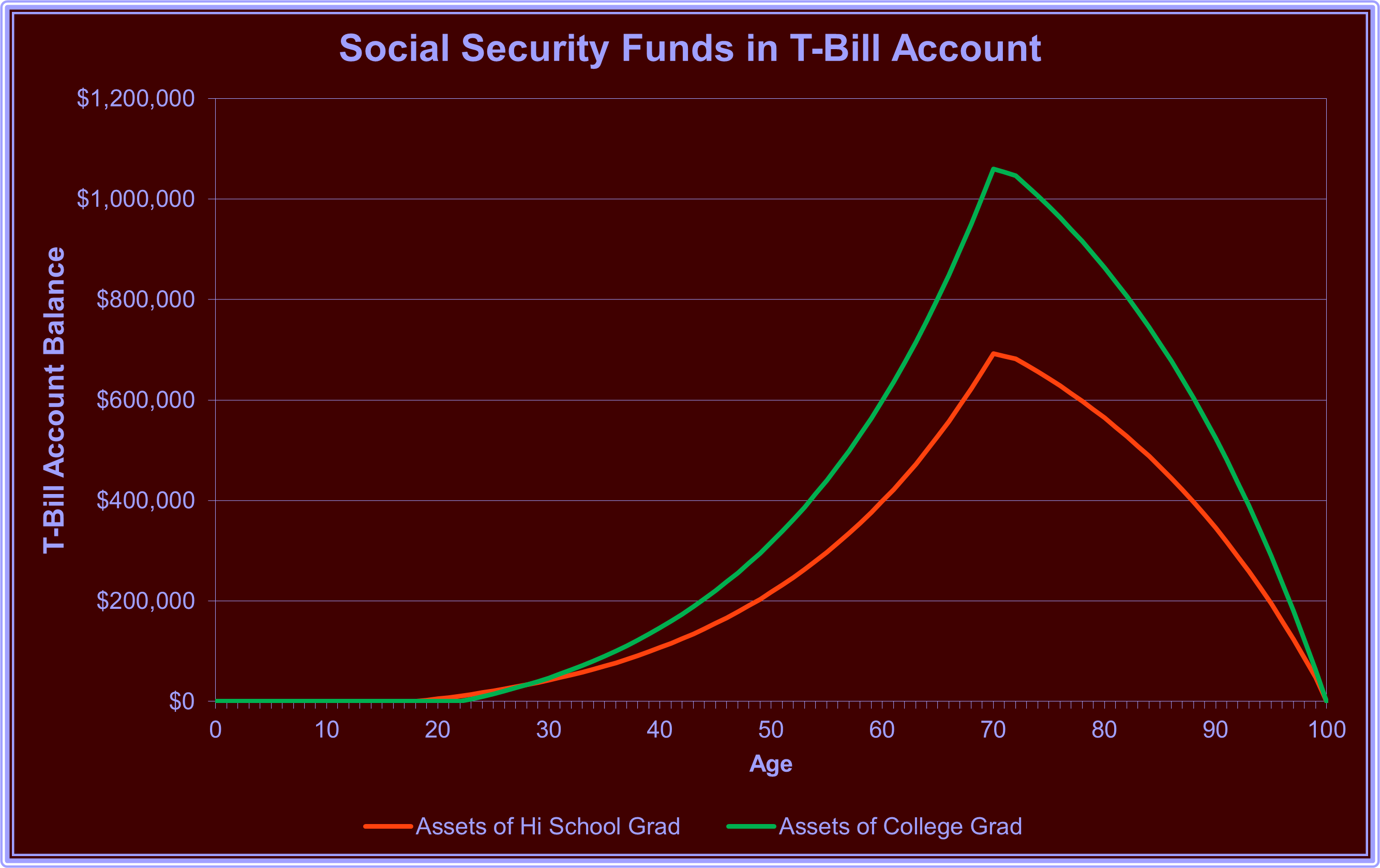

There's been talk for decades about how to fix social security. We're still waiting. Some say the answer is higher taxes; others say privatization. I have a solution that may satisfy everyone. Continue to assess the 12.4% combined employer-employee payroll tax, but don't put it in the current Social Security Trust Fund. Instead, create an individual account for every worker and invest it in 3-month US Treasury bills (T-bills). This method is a way to 'sort of' privatize without the associated risks that might come with putting it in the stock market. With their historical average return of 4.46%, T-bills provide a secure and stable investment, instilling confidence in the system's financial security. Since everyone has their own account, everyone gets out what they personally contributed, plus interest. Since it is a personal account, the balance can be passed to survivors after death. This means that if the account holder does not survive to 100, their heirs could take the remaining balance as a lump sum, or they could elect to continue to receive the payout until what would have been an age of 100. This inheritance feature provides a safety net for families. It also offers higher payouts due to the more favorable interest rate. Why hasn't this been done already? By putting the money in a single fund, Congress can fiddle with it—and it does. The Congress is always averse to giving up the power to control things. In the chart below, you can see how the money in an individual account grows. The red line shows a hypothetical high school graduate who began working at eighteen with a starting salary of $20,000/year and worked until age seventy. The green line shows a hypothetical college graduate who started working at twenty-two with a starting salary of $38,000/year and continued until age seventy. At age seventy, the high school grad begins withdrawing from the account at a rate of 3583.33 monthly. Under the current system, the average retiree who retires at seventy receives $2037.54 monthly. At age seventy, the college grad starts withdrawing $5516.67 monthly. The current Social Security maximum benefit is $5108 monthly.

As you look at the chart, you can see it goes to age 100. If the account holder does not survive to 100, you can see on the chart the amount that their heirs could take as a lump sum, or they could elect to continue to receive the payout until what would have been an age of 100. So, this system results in higher benefits, removes the temptation for Congress to tamper with the funds in the accounts, and carries a death benefit that the current system generally does not. However, the most significant advantage is that each account holder's money is truly their money and does not rely upon future generations to keep the system solvent. Frankly, I'm not optimistic about Congress giving up its power over the trust fund as it exists in the current system, but if we don't try, we will never get the system we deserve. It's our money; we have the right to own and control it.

If you found this article stimulating, please share it with other folks who might enjoy it. And please share your thoughts below. Dr. Cardell would love to hear from you.

Questions, Comments, Criticisms, or Witty Remarks:

Recent Articles

Newest to Oldest

Contact Us

Dr. Doug would love to hear from you:

Copyright © 2018 - 2026 DougCardell.com. All rights reserved.

![[Valid RSS]](valid-rss-rogers.png "Validate my RSS feed")

Responses